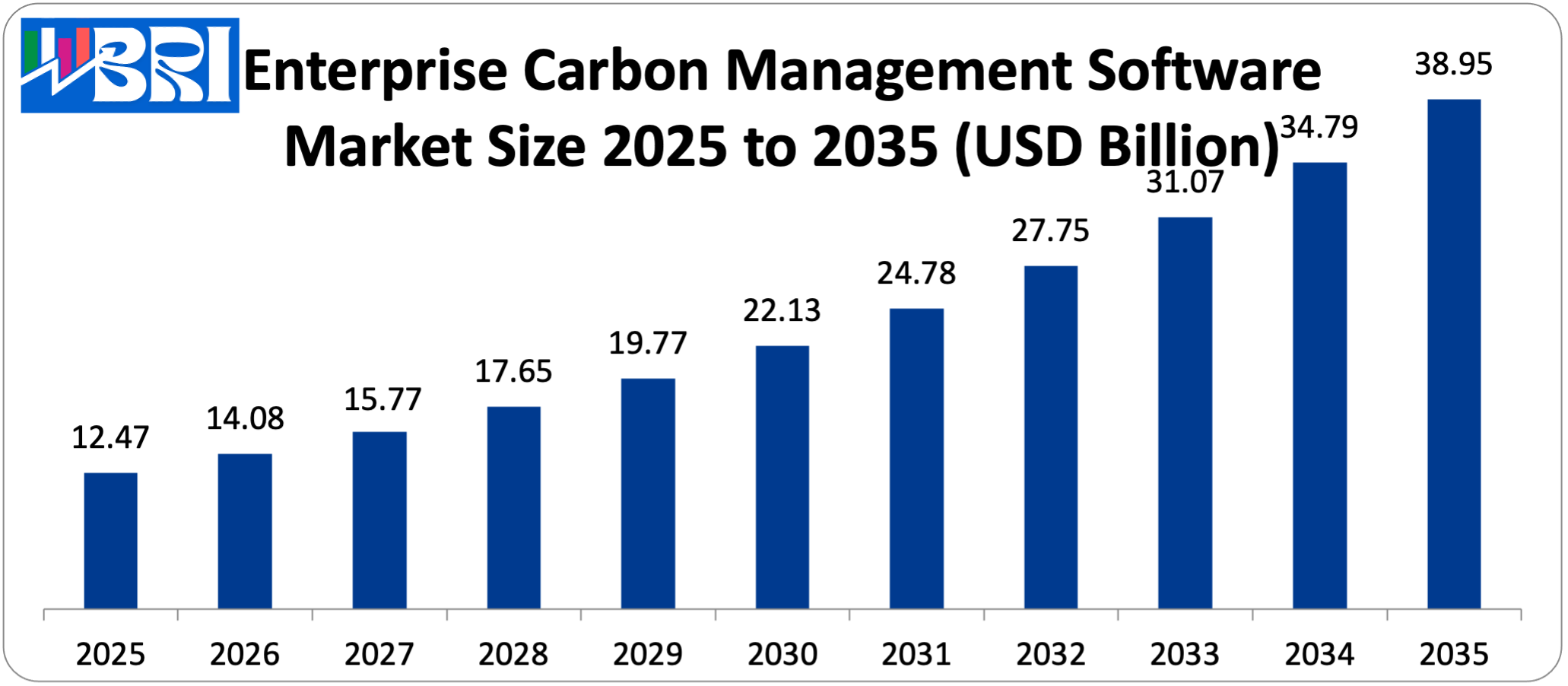

The worldwide enterprise carbon management software market size is estimated at USD 12.47 billion in the year 2025 and is simulated to rise between USD 14.08 billion in the year 2026 to estimated USD 38.95 billion between the year 2026 and 2035 at a CAGR of 12.9%.

Enterprise Carbon Management Software Market Revenue and Trends

Enterprise carbon management software markets offer a global environment to measure, track, report, and reduce greenhouse gas emissions at Scopes 1, 2, and 3, be it in compliance, ESG reporting, and decarbonization policies. The worldwide enterprise carbon management software sector is expanding progressively, owing to the augmenting regulatory requirements, expanding corporate net-zero pledges, heightened investor attention on ESG execution, and improvements in AI-powered analytics and cloud-based applications in sustainability ecosystems the world over.

What are the Factors That Have a Significant Contribution to the Growth of the enterprise carbon management software market?

Demand in carbon management software products has risen in response to the increased number of organizations requiring to comply with mandatory carbon disclosure regulations, including CSRD in Europe and plans to regulate net-zero disclosure in the US, as well as voluntary carbon management pledges and supply chain pressure. With the introduction of global emissions reporting as a norm and the increased pressure of Scope 3, additional enterprises will be interested in automated products to measure and plan reductions and prepare to audit and report.

The technology has brought with it new innovations such as AI-driven data automation, predictive decarbonization simulation, integration of IoT to track in real-time and generative AI to analyze scenarios to increase accuracy and user compliance. Others involve the ESG metrics focus on investor relations, the wider application of the SMEs through lower-priced SaaS models, and government support of sustainability and climate disclosure schemes in both developed and emerging markets.

Segment Insight

By Product Type

Through products, cloud-based enterprise carbon management products owned by far the largest portion of the enterprise carbon management software market as of 2025 due to demand of scalable platforms that enable automated calculation of emissions, ESG reporting, and Scope 3 data management, and remain innovated in the use of AI and SaaS products mentioned by large percentages of users as better at improving the efficiency of compliance and decarbonization outcomes.

By Distribution Channel

The biggest market share is among direct sales and SaaS subscription platforms which are key platforms of enterprise deployments, bespoke integrations, and continuing advisory services. Being able to offer professional capabilities toward regulatory alignment, data validation, and more specific decarbonization processes of organizations with complicated emissions profiles, they have gained popularity as a choice of implementing carbon management platforms.

Regional Insights

The North American marketplace dominates the world market in terms of enterprise carbon management software owing to its strict regulatory controls, understanding of the non-financial requirements of environmental sustainability, and implementation of more advanced sustainability software. Strong disclosure regulations, such as SEC proposals, pervasive corporate net-zero ambitions, and early adoption of AI and cloud functionality are advantages to North America as well. The existence of key players in the industry and the current level of innovation and pressure by investors all aid the further dominant role of North America.

Besides, the Asia Pacific region is recording the worst growth in the enterprise carbon management software market due to a rapid industrialization, growing corporate sustainability obligations, and stricter enforcement of regulations on emissions. Adoption of carbon management platforms has been observed to gain significant momentum in China, India, and Japan as affordability continues to increase, there is greater awareness of ESG and decarbonization programs are supported by the government. The green finance, supply chain transparency, and digital transformation in this region will increase at a high rate in the Asia Pacific market.

Report Scope

| Feature of the Report | Details |

| Market Size in 2026 | USD 14.08 billion |

| Projected Market Size in 2035 | USD 38.95 billion |

| Market Size in 2025 | USD 12.47 billion |

| CAGR Growth Rate | 12.9% CAGR |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Key Segment | By Component, Deployment Mode, Organization Size, Application, End-User Industry and Region |

| Report Coverage | Revenue Estimation and Forecast, Company Profile, Competitive Landscape, Growth Factors and Recent Trends |

| Regional Scope | North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America |

| Buying Options | Request tailored purchasing options to fulfil your requirements for research. |

Recent Developments

- In October 2025: Greenly launched EcoPilot, a new AI-powered carbon accounting platform that automates data collection, emissions-factor assignment, and enables modeling of Scope 3 reductions with “what-if” scenarios for net-zero planning.

List of the prominent players in the Enterprise Carbon Management Software Market:

- Salesforce Inc. (Salesforce Net Zero Cloud)

- SAP SE (SAP Cloud for Sustainable Enterprises)

- Microsoft Corporation (Microsoft Cloud for Sustainability)

- IBM Corporation (IBM Environmental Intelligence Suite)

- Workiva Inc.

- Wolters Kluwer (Enablon)

- Sphera Solutions Inc.

- Schneider Electric (EcoStruxure Resource Advisor)

- ENGIE Impact

- Persefoni AI Inc.

- Plan A

- Sweep

- Others

The Enterprise Carbon Management Software Market is segmented as follows:

By Component

- Software

- Carbon Accounting Software

- Emissions Tracking Software

- Reporting and Analytics Software

- Services

- Professional Services

- Managed Services

By Deployment Mode

- Cloud-based

- On-premise

- Hybrid

By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

By Application

- Carbon Accounting and Reporting

- Emissions Tracking and Monitoring

- Sustainability Reporting

- Supply Chain Carbon Management

- Carbon Offsetting and Trading

- Other Applications

By End-User Industry

- Manufacturing

- Energy and Utilities

- Transportation and Logistics

- Retail and Consumer Goods

- Information Technology

- Financial Services

- Other Industries

Regional Coverage:

North America

- U.S.

- Canada

- Mexico

- Rest of North America

Europe

- Germany

- France

- U.K.

- Russia

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- New Zealand

- Australia

- South Korea

- Taiwan

- Rest of Asia Pacific

The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America

[embedsocial_reviews id=”d4ae80cffae3d938f997111953699a733c8e6f99″]